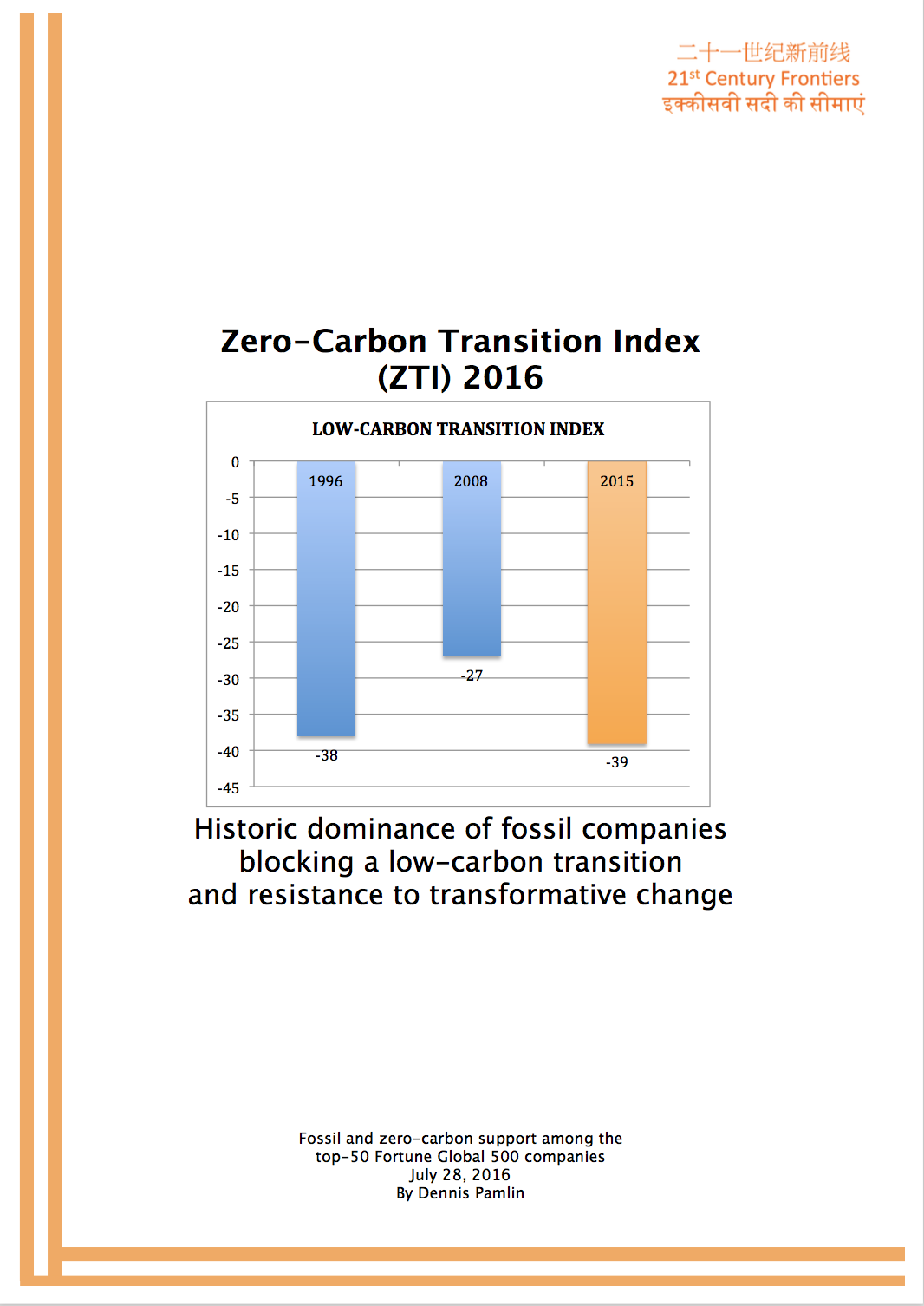

Zero-Carbon Transition Index (ZTI) 2016

/Role: author

Summary

As the world moves into implementation of the Paris agreement, an agreement that is notoriously vague even by international environmental agreements standards, it is important to understand the broader context for a transition to a zero-carbon society. One of the most important factors that will decide the outcome of the Paris agreement is the kind of stakeholder that will influence the international agenda.

There are many ways that different stakeholders can influence the international agenda in many different ways, but based on historic experience international media, leading policy makers, key academic institutions, international organizations, etc. will act very much in line with the companies that are the most powerful and the agenda they promote.1 These companies does not only have significant investments in R&D and enormous PR /lobby budgets, they are also overrepresented in key fora, including industry groups and agenda-setting processes such as OECD, B20, and WEF.

Currently, and perhaps surprisingly, the domination by pro-fossil companies among the world’s top-50 companies is record high. The situation today is even worse than back in 1996, when the Kyoto protocol was negotiated. In other words, 20 years of negotiations, discussions and actions to reduce global carbon emissions have failed to deliver a new generation of proactive zero-carbon companies on the same scale as the old fossil companies. What we have today is a situation when the top-50 companies on the planet are dominated by fossil friendly companies on an unprecedented scale.

The zero-carbon transition index (ZTI) is a tool to enhance transparency regarding how biggest companies on the planet are likely to use their influence. The ZTI uses the revenue data from Fortune Global 500 to select the top-50 companies in the world as measured by revenue.2 These companies are then divided into five categories depending on how they invest, communicate and lobby with regards to the greenhouse gas (GHG) reductions needed to avoid dangerous climate change.

The five categories are “very obstructive”, “obstructive”, “neutral”, “supportive”, and “very supportive”. The companies in the category very obstructive are given the value -100, the obstructive -50, the neutral 0, the supportive +50, and the very supportive +100. The values are added together and then divided by the total number of companies to get the ZTI.

The ZTI for 1996 was -38, for 2008 -27 and now for 2015 it is -39.